[ad_1]

Carve-outs, take-private offers, industrial upgrading and demographic shifts are anticipated to revive Asia’s personal fairness market from a slowdown since 2021.

Valuations have adjusted downward, creating extra engaging entry factors, whereas ongoing company restructuring is about to spice up buyout demand. The reopening of IPO home windows will pave the best way for improved exit opportunies, amid rising market liquidity.

Portfolio rebalancing by world traders, at present underweight within the area, is predicted to bolster the area’s buyout market, pushed by its strong fundamentals, StepStone stated.

Asia personal fairness funds have outperformed the MSCI AC Asia Index by 4-8% inner fee of returns throughout most vintages since 2010, delivering extra secure returns than public markets, even throughout macro downturns, Vincent Hsu, companion at StepStone Group, stated throughout a roundtable dialogue hosted by The Korea Financial Each day on Nov. 7 .

“The sustained efficiency premium highlights the structural benefits of personal markets in Asia, together with entry to early development, founder transitions and operational worth creation. This reinforces the case for strategic allocation to Asia PE as a long-term return driver.”

StepStone notes a shift towards sectoral focus, particularly in expertise, industrial upgrading, healthcare and client companies, together with elevated secondary transactions for liquidity administration.

On the draw back, the depreciation of most Asian currencies might heighten international change threat, requiring traders to undertake selective hedging methods.

By nation, engaging carve-out alternatives from family-run conglomerates are rising in South Korea.

“In Korea, typical playbook right here for personal fairness has typically been the chaebol carve-outs. There are massive hopes that the value-up program or reforms can truly mirror what you noticed in Japan,” Hsu stated.

Chaebol is a Korean time period referring to massive, family-run conglomerates established within the early to mid-1900s.

In February, StepStone co-invested in SK Microworks, a unit of South Korea’s No. 2 conglomerate, with Seoul-based personal fairness agency Hahn & Co.

In Japan, take-private alternatives are on the rise as listed small and medium-sized enterprises, which signify round 70% of whole employment, commerce at engaging valuations.

Strengthening company governance requirements and rising activist shareholder engagement are including additional momentum to non-public fairness exercise and worth creation.

In India, personal fairness exit values are rising, supported by favorable demographics and a quickly client base, with roughly 40% of the inhabitants aged between 20 and 40.

“In India, there’s extra exit alternatives … Japan is a brilliant spot for Asian personal fairness. There are a whole lot of tailwinds due to the development in company governance in addition to… extra activist shareholders.”

In China, IPO actions are rebounding to ranges nearing the 2021 peak. Nonetheless, the market stays underneath correction as a result of regulatory uncertainty and weaker investor sentiment, Hsu cautioned.

In Australia, sturdy buyout alternatives are rising within the lower- to mid-market phase, significantly throughout healthcare, expertise and business-to-business companies.

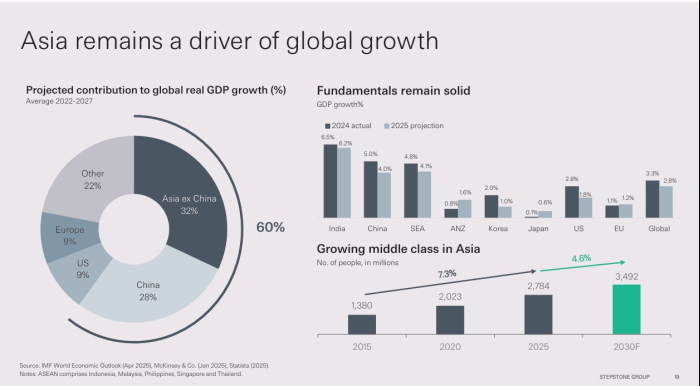

Asia contributes about 60% of world inflation-adjusted GDP development between 2022 and 2027, with China alone accounting for round 28%, in accordance with the IMF World Financial Outlook.

StepStone has invested about $14 billion in Asia’s PE market since 2019. It evaluations over 4,000 funding alternatives yearly throughout personal fairness, actual property, infrastructure, and personal debt by primaries, secondaries, and co-investments.

World PE distributions in 2025 are round 5% of internet asset worth, nicely under the long-term common of 21%, reflecting slower exits, in accordance with StepStone.

[ad_2]